At first glance, the US machine vision market appears highly consolidated.

The top three vendors account for nearly half of total market revenues, giving the impression of a market increasingly dominated by a handful of major players. Yet beneath that surface sits a surprisingly fragmented ecosystem of smaller suppliers, many of them deeply specialized in narrow industrial applications.

According to new analysis from Interact Analysis, this apparent contradiction is one of the defining characteristics of the US machine vision landscape in 2025.

The question now is whether the market will continue consolidating around large multi-sector vendors, or whether specialized niche players will continue carving out defensible positions in smaller applications.

A Market That Is Both Concentrated and Fragmented

Valued at approximately $980 million in 2025, the US machine vision market is shaped by two opposing dynamics:

- a small group of dominant vendors,

- and a long tail of specialized suppliers.

The top three vendors collectively account for around 45% of total market revenues, driven largely by their positions in major sectors such as:

- logistics,

- automotive,

- and large-scale industrial automation.

On paper, that level of concentration resembles a mature industrial market consolidating around scale, but the broader competitive picture is more nuanced. Beyond the largest suppliers sits a fragmented network of smaller vendors focused on highly specialized applications, often serving industries with unique technical requirements, regulatory constraints, or deployment conditions.

These niche positions create strong barriers to entry and allow smaller players to remain highly competitive within specific sectors.

In other words:

while the overall market looks concentrated, many individual sectors remain dominated by specialized expertise.

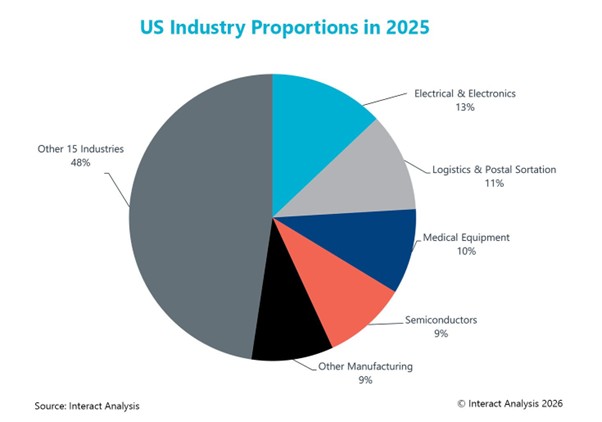

Sector Composition Explains the Long Tail

One of the key insights from the research is that vendor concentration closely mirrors the composition of industries using machine vision.

The US market consists of:

- a few very large industries,

- alongside a large number of smaller vertical applications.

Of the 20 sectors analyzed by Interact Analysis:

- just five sectors account for more than 9% of total market demand,

- while eight sectors contribute less than 2% each.

This creates a structure where:

- large vendors dominate the largest industries,

- while smaller vendors maintain stronger positions in smaller, highly specialized markets.

The result is a market that simultaneously supports:

- large platform-oriented suppliers,

- and highly focused technical specialists.

Why Large Vendors Continue to Gain Ground

The critical question is whether this balance remains stable. According to Interact Analysis, current growth forecasts suggest the market is likely to become more concentrated over time.

The reason is relatively straightforward:

the largest machine vision sectors are expected to grow faster than the smallest niche applications.

The four largest sectors, each accounting for more than 10% of the market, are forecast to grow at a combined CAGR of 11%.

By contrast, the nine smallest sectors, each representing 2% or less of the market are projected to grow at a combined CAGR of 9%. That gap may appear modest, but over time it increasingly favors vendors already dominant in large-scale automation sectors.

In effect, the structure of market demand itself is reinforcing consolidation.

Acquisitions Are Accelerating the Trend

Beyond organic growth dynamics, acquisitions are also reshaping the competitive landscape. Recent transactions show machine vision vendors increasingly using M&A to:

- enter new verticals,

- acquire technical competencies,

- strengthen positions in high-growth applications,

- and expand platform capabilities.

Examples highlighted in the research include:

Teledyne + FLIR

Teledyne’s acquisition of FLIR strengthened its position in:

- thermal imaging,

- safety,

- defense,

- and industrial sensing applications.

Basler + Roboception

Basler’s acquisition of Roboception expanded its capabilities in:

- 3D imaging,

- robotics,

- logistics,

- and automotive automation.

Teledyne + Adimec

Teledyne’s acquisition of Adimec helped strengthen its competencies in:

- healthcare imaging,

- high-performance industrial imaging,

- and defense applications.

TKH Group + Euresys

TKH Group’s acquisition of Euresys enabled expansion into applications requiring:

- high frame-rate imaging,

- advanced vision processing,

- and more complex inspection workflows.

Taken together, these moves suggest that consolidation is no longer simply about scale. It is increasingly about acquiring specialized capabilities that would be difficult, expensive, or time-consuming to develop internally.

The Market Is Shifting Toward Platforms

One broader implication emerging from these trends is that machine vision is increasingly behaving like a platform market rather than a pure component market.

Larger vendors are expanding beyond cameras and sensors into:

- software,

- AI tooling,

- 3D vision,

- thermal imaging,

- logistics systems,

- robotics integration,

- and application-specific solutions.

This creates stronger ecosystem lock-in and makes it harder for smaller standalone vendors to compete broadly across multiple sectors.

At the same time, niche suppliers with deep technical expertise may continue thriving in specialized areas where:

- performance requirements are unique,

- integration complexity is high,

- or customer relationships remain highly application-specific.

The result is likely not total consolidation, but a widening divide between:

- large multi-domain platform providers,

- and focused niche specialists.

Final Thoughts

The US machine vision market is becoming more concentrated — but not uniformly so.

Large vendors continue strengthening their positions through:

- faster growth in major automation sectors,

- platform expansion,

- and targeted acquisitions.

Yet the industry still supports a broad ecosystem of smaller specialists serving narrower applications with strong technical barriers to entry.

For the foreseeable future, the market may continue operating with both dynamics simultaneously:

concentration at the top, fragmentation at the edges. And as automation investment increasingly shifts toward integrated systems rather than standalone components, the vendors best positioned for long-term growth may be those capable of combining scale, software, imaging, and application expertise into unified industrial platforms.

About the Author

Jonathan Sparkes is a Market Analyst at Interact Analysis, specializing in industrial automation and machine vision markets.

This article was adapted and edited for publication by MVPro Media based on analysis provided by Interact Analysis.