By Mark Williamson

This is the time of year when most companies are deep into planning cycles, reviewing performance, adjusting strategy, and setting targets for the year ahead. The intention is always the same: do more of what worked, fix what didn’t, and position the business to outperform the market. In an industry like machine vision, where long-term growth has consistently exceeded broader manufacturing trends, strong market expansion can sometimes mask underlying weaknesses. When the tide is rising, even average companies can appear to be sailing smoothly.

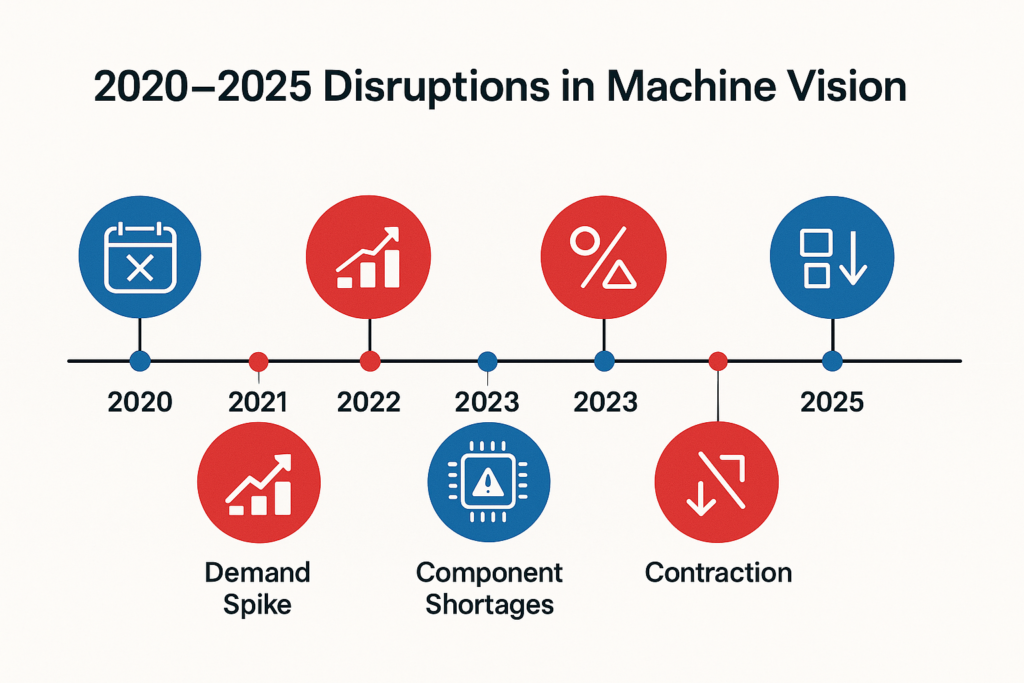

For more than a decade, machine vision has delivered impressive growth. VDMA trade association data shows a European CAGR of around 9% since 2013, with only one year of decline: a 4% drop in 2020 as the pandemic brought manufacturing to a halt. The rebound was equally sharp with 2021 surging by 17%, the strongest year in the same period with continued growth in 2022. Yet the period that followed has been defined not by steady expansion, but by volatility unlike anything I’ve seen in more than 30 years in the industry. The question now is whether the uncertainty of recent years is finally easing as we look toward 2026.

From Pandemic Shock to Component Chaos

To understand where we’re heading, we need to revisit the years that reshaped the industry.

The initial downturn in 2020 was no surprise. The pandemic caused global factory shutdowns which halted production, orders and shipments per postponed or cancelled and capital investments paused. But as manufacturers scrambled to recover lost output, demand snapped back faster than supply chains could respond. Component shortages, many caused by surging consumer electronics demand from home working quickly became critical. Semiconductor foundries at full capacity prioritised high-volume markets, sidelining niche products like machine vision sensors. FPGA (Field-Programmable Gate Array )manufacturers even cancelled long-standing product lines with little warning, leaving camera makers no choice but to redesign hardware almost overnight.

The shockwaves from this period still echo today. Major OEM customers, desperate to secure continuity, bought up global stock. Lead times ballooned beyond 12 months, and in some cases, components were discontinued entirely. Engineering teams that would normally drive innovation spent their time firefighting redesigns. The result was a slowdown in forward-looking R&D and a bottleneck in product introductions that stretched across multiple years.

A Perfect Storm of Economics and Geopolitics

Just as the supply chain began to stabilise, inflation surged. Central banks responded with rapid interest rate hikes that froze capital investment, the lifeblood of many machine vision OEMs. At the same time, geopolitical tensions escalated, adding further uncertainty.

Many machine vision company leaders have told me the same story: they didn’t lose customers, but orders were delayed or paused while OEMs worked through overstocked inventories. Europe felt this most acutely. According to VDMA, the machine vision market fell 7% in 2023 and a further 10% in 2024, with components hit harder than system integrators due to the high levels of component inventories. Interact Analysis a market research company who understand the industry well reported global declines of 2.8% and 3.9% for the same years, while A3 trade association data suggested the U.S. shrank just 1% highlighting a widening gap between regional trajectories.

2025: A Year of Conflicting Signals

As 2025 began, there was cautious optimism. Inventory levels were normalising, interest rate cuts were being discussed, and several analysts forecast stabilisation. VDMA projected a flat year for Europe; Interact Analysis predicted modest global growth of 1.5%, with a more robust recovery beginning in 2026 and a return to historical growth rates in 2027.

Then came the introduction of U.S. tariffs—another source of uncertainty that disrupted early forecasts.

Industry indicators since then have been mixed. EMVA trade association data showed continued revenue contraction in Q2 2025, even as member companies expressed positive outlooks. VDMA reported bookings down 1% in the first nine months of the year, but billings up 9%.

Looking at publicly traded machine vision companies in the first 9 months of the year Teledyne Technologies digital imaging segment reported a global revenue increase of 2.9%, TKH group machine vision sector growth of 11.4%, Cognex increasing13% however projecting a slower last quarter growth of 3% and Basler posted a striking 23% increase in revenue and 29% growth in orders, though it acknowledged that Europe remained its slowest region, with recovery driven primarily by China and the U.S. While Basler’s results look impressive we need to remember Basler had the most severe contraction between 2021 and 2023, largely due to its higher reliance on the Chinese market during a period of sharp slowdown there. The narrative at the time was that maturing local competitors would increasingly squeeze western component suppliers. Yet 2025 saw China rebound strongly. In my view, this is partly due to de-globalisation pressures: Chinese capital equipment manufacturers need western components for export markets due to import controls effecting in high-growth sectors like battery manufacturing where Chinese companies lead the market. This has created renewed opportunities for European suppliers.

Still, with VDMA revising its 2025 projection to “flat at best” and broader automation markets expected to contract, the signals remain contradictory. Conversations with industry leaders and review of published reports suggest that growth is returning, but unevenly. Agile companies with strong product portfolios or exposure to growth verticals are outperforming the pack, while others remain in a holding pattern. Three years on, we are still far from the highs of 2022, this has been the longest period of stagnation I can recall.

The Outlook for 2026

So where does this leave us?

I expect 2026 to deliver growth, but not a return to the long-term 9% CAGR the industry enjoyed in the preceding decade. Europe will again trail global performance, influenced by slower capital investment cycles and a higher administrative burden compared with other regions.

Several themes stand out:

• 3D machine vision remains the strongest hardware growth segment.

Demand is rising across logistics, robotics, and quality inspection. Competition is intensifying, which will apply downward pricing pressure, but market expansion should offset much of this.

• Sector-specific momentum will vary.

Battery manufacturing and logistics continue to show the highest sustained growth. Non-industrial applications such as medical imaging and smart agriculture are expanding more quickly than traditional factory automation segments.

• Innovation will be a differentiator again.

With engineering teams no longer tied up in redesigns, companies that invest in true product development, not just iterations will outperform. There is ample room for disruption, particularly in software and edge processing.

• Investment interest will remain solid.

Machine vision still offers above-average growth potential, strong margins, and significant value-creation opportunities in the supply chain. It is not yet commoditised, despite increasing competition.

• Consolidation will continue, but at a slower pace.

Financial pressures over the past few years have encouraged merger & acquisition activity, but the pool of founder-led independents is shrinking. Consolidation will remain a feature of the landscape just not at the frenetic pace seen immediately before and during the pandemic.

Closing Thoughts

The past few years have tested the machine vision industry in ways few anticipated. Component shortages, geopolitical instability, economic headwinds, and shifting global demand patterns created a level of volatility unmatched in recent memory. Yet the fundamentals remain robust. Machine vision continues to expand into new sectors, new applications, and new geographies.

2026 will not bring a dramatic snapback to historic growth levels, but it does mark the beginning of a more stable phase. For companies willing to innovate, adapt quickly, and focus on high-value segments, the coming years will offer strong opportunities.

After a long period of turbulence, the industry is finally finding its footing again. And while the crystal ball is still a little cloudy, the direction of travel is becoming clearer.